External trade - 2 quarter

Product Code: q-6032-09

In the first half of 2009, external trade turnover 1 showed the largest decline 2 in the history of the Czech Republic . Given the significant year-on-year drop in exports and particularly imports, the external trade turnover fell by 20.3% compared to the first half of 2008 (as opposed to +6.6% in the first half of 2008 compared to the first half of 2007). In the first half of 2009, the trade balance posted the largest surplus 3 (CZK 79.4 billion) since 2005, when external trade showed a surplus for the first time in the history of the Czech Republic, with surpluses being typical of all the subsequent years.

In the first half of 2009 compared to the first half of 2008:

- exports were down by 19.2% (CZK 249.5 billion) and reached CZK 1,048.4 billion; imports were down by 21.5% (CZK 264.8 billion) and reached CZK 968.9 billion. Exports and imports fell more significantly in Q2 2009 (by 19.7% and 22.9% respectively) than in Q1 2009 (by 18.8% and 20.0% respectively). The drop in exports and imports accounted for 48.5% and 51.5% respectively of the year-on-year decline in the external trade turnover by CZK 514.3 billion. Due to the significant depreciation of CZK against EUR and notably USD 4 , exports and imports expressed in those currencies declined more heavily year-on-year in comparison with the decline in CZK. Exports and imports expressed in EUR fell by 25.0% and 27.1% respectively while exports and imports expressed in USD were down by 34.8% and 36.6% respectively;

- external trade surplus increased by CZK 15.3 billion and reached CZK 79.4 billion (the rate of coverage of imports by exports was 108.2% in the first half of 2009, as opposed to 105.2% in the first half of 2008). The trade balance surplus was higher in Q2 2009 (CZK 44.1 billion) than in Q1 2009 (CZK 35.3 billion). By group of countries, the trade surplus with EU countries fell by CZK 18.1 billion while the trade deficit with non-EU countries decreased by CZK 33.4 billion. The trade surplus with EFTA countries fell by CZK 4.6 billion while the trade surplus with European transition economies was down by CZK 1.7 billion. The trade deficit with CIS 5 went down by CZK 29.0 billion, with developing economies by CZK 7.2 billion, with other developed market economies by CZK 4.8 billion and with other countries 6 by CZK 2.8 billion. By commodity section, the surplus of external trade in ‘manufactured goods classified chiefly by material’ grew by CZK 13.5 billion while it fell by CZK 28.1 billion in ‘machinery and transport equipment’ and by CZK 6.9 billion in ‘miscellaneous manufactured articles’. The deficit of external trade in ‘crude materials, inedible, and mineral fuels’ decreased by CZK 32.4 billion and the trade deficit in chemicals fell by CZK 8.0 billion while the trade deficit in ‘agricultural and food crude materials and products’ grew by CZK 3.6 billion;

- by group of countries, the share of EU countries in total exports dropped from 85.7% to 85.0%, and more markedly in overall imports, from 68.5% to 66.2%. In total exports, shares of EFTA countries increased (from 1.9% to 2.3%), as did the shares of developing economies (from 3.2% to 3.9%), other developed market economies (from 3.5% to 3.8%) and other countries (from 0.6% to 0.7%); the shares of CIS countries and European transition economies decreased from 3.8% to 3.4% and from 1.0% to 0.8% respectively. In total imports, the shares of EFTA countries grew from 1.5% to 2.3%, as did the shares of other developed market economies from 6.7% to 7.4%, developing economies from 5.9% to 6.7% and especially other countries from 8.0% to 9.9%. The share of CIS declined from 8.7% to 6.7% and that of European transition economies decreased from 0.4% to 0.3%;

- by commodity section, in total exports, the shares of ‘machinery and transport equipment’ decreased from 54.7% to 53.4% and of ‘manufactured goods classified chiefly by material’ fell from 19.7% to 18.2%; shares of ‘agricultural and food crude materials and products’, ‘chemicals and related products’, ‘crude materials, inedible, and mineral fuels’ and ‘miscellaneous manufactured articles’ increased. In total imports, shares of ‘machinery and transport equipment’ dropped from 41.8% to 40.8%, as did the shares of ‘manufactured goods classified chiefly by material’ from 20.4% to 17.9% and of ‘crude materials, inedible, and mineral fuels’ from 12.6% to 11.2%. The shares of ‘agricultural and food crude materials and products’ in total imports grew from 4.8% to 6.4%, as did the shares of ‘chemicals and related products’ from 10.5% to 11.3% and ‘miscellaneous manufactured articles’ from 9.9% to 12.4%.

The main impacts on external trade in the first half of 2009 included:

- A fall in industrial production, which hit all manufacturing industries. The decrease in the output of manufacturing industries affected total exports. In the first half of 2009, compared to the first half of 2008, the exports of the manufacturing industry 7 fell by 20.3% (CZK 253.7 billion) and its share of total exports declined to 95.2% from 96.5% in the first half of 2008.

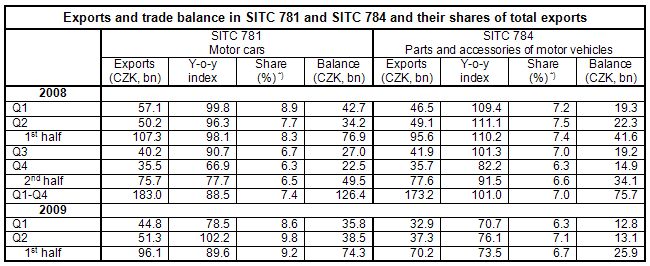

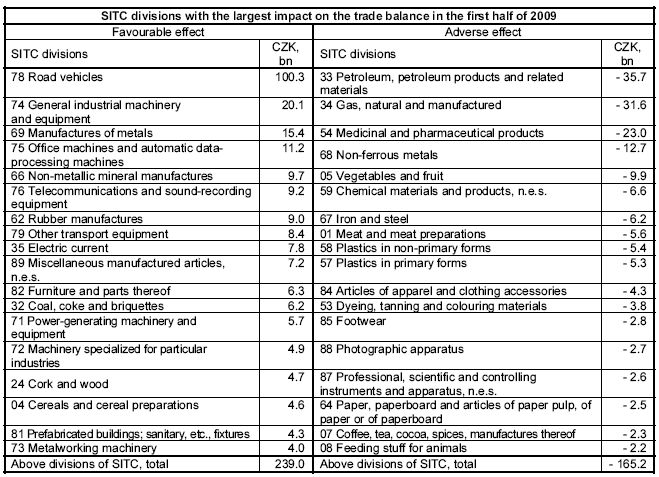

The most important sections of manufacturing exports in the first half of 2009 continued to include primarily ‘machinery and transport equipment’, especially ‘road vehicles’, ‘electrical machinery, apparatus and appliances’, ‘office machines and automatic data-processing machines’, ‘general industrial machinery and equipment’, and ‘telecommunications equipment’. Exports of ‘road vehicles’ made up 16.9% of all exports in the first half of 2009 (17.0% in the first half of 2008), of which ‘motor cars’ made up 9.2% and ‘parts and accessories for motor vehicles’ 6.7%. While external trade in road vehicles still produced the highest surplus among all sections of SITC in the first half of 2009 (CZK 100.3 billion), the surplus fell by CZK 9.7 billion y/y (down by CZK 2.6 billion in ‘motor cars’ and by CZK 15.7 billion in ‘parts and accessories for motor vehicles’).

*)Share (%) in total exports in given period.

The second largest (CZK 20.1 billion), yet by CZK 6.9 billion y/y lower, surplus in machinery trade (and also in total external trade) was posted by ‘general industrial machinery and equipment’;

- Significantly weakened external demand, due to the global financial and economic crisis. Particularly the significant economic slowdown of EU countries and the related decline in demand in those countries affected the Czech Republic’s external trade. The downturn of the German economy, which is the most important export destination for Czech businesses, was of key importance. Exports to Germany fell by 12.8% y/y in the first half of 2009;

- Favourable terms of trade 8 . The fluctuation of external trade prices was influenced by world market prices and exchange rates of CZK against EUR and USD. In January-May 2009, compared to the same period of 2008, export prices were up by 3.6% on average and import prices were down by 0.1% on average while terms of trade reached +103.7. In the said period, exports and imports decreased by 20.1% and 21.9% respectively at current prices, and by 22.4% and 22.5% respectively at constant prices. In January-May 2009, prices raised the exports at current prices by almost CZK 25 billion and the imports in current at by more than CZK 6 billion. External trade surplus at constant prices was nearly CZK 19 billion lower than the external trade surplus at current prices.

A closer look at external trade by group of countries in the first half of 2009 shows that, on the year-on-year basis:

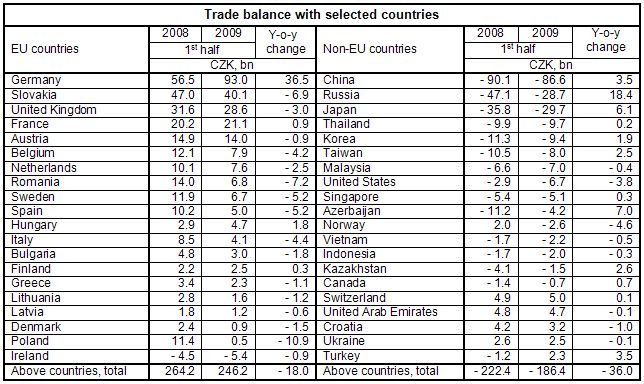

- Exports decreased to all groups of countries. Exports to EU countries declined by 19.9% (CZK 221.5 billion) while exports to non-EU countries were down by 15.1% (CZK 28.0 billion). The largest relative year-on-year decline was obvious in the exports to European transition economies and the CIS, followed by other developed market economies and other countries, and by developing economies; exports to EFTA countries fell to the smallest extent. The decline in exports to EU countries in total reflected the fall in exports (except Malta) to all EU countries. The largest absolute decline was shown in the exports to Germany (CZK 51.0 billion), followed by Slovakia (CZK 23.6 billion), Poland (CZK 23.2 billion), Italy (CZK 18.1 billion), the United Kingdom (CZK 14.2 billion), France (CZK 12.5 billion) and Austria (CZK 12.2 billion). As far as non-EU countries are concerned, exports to Russia decreased (CZK 7.8 billion), as did the exports to Ukraine (CZK 5.4 billion) and the Untied States (CZK 3.9 billion). Exports to Turkey (CZK 2.4 billion) and Norway (CZK 1.9 billion) went up;

- Imports from all groups of countries except EFTA States decreased. Imports from EU countries were down by 24.1% (CZK 203.4 billion) while imports from non-EU countries fell by 15.8% (CZK 61.4 billion). The most significant relative decline was evident in the imports from European transition economies and the CIS, followed by other developed market economies and developing economies; imports from other countries fell to the smallest extent. Imports from EFTA States went up. The decline in imports from EU countries in total reflected lower imports from almost all EU countries (except Malta, Latvia and Ireland). Significant year-on-year decreases were obvious in the imports from Germany (CZK 87.5 billion), followed by Slovakia (CZK 16.7 billion), Italy (CZK 13.7 billion), France (CZK 13.4 billion), Hungary (CZK 12.6 billion), Poland (CZK 12.3 billion), Austria (CZK 11.3 billion) and the United Kingdom (CZK 11.2 billion). As regards non-EU countries, imports particularly decreased from Russia (CZK 26.3 billion), Japan (CZK 7.9 billion), Azerbaijan (CZK 7.2 billion), Ukraine (CZK 5.3 billion) and China (CZK 3.7 billion). Imports from Norway went up (CZK 6.5 billion);

- External trade surplus grew. The trade surplus with EU countries reached CZK 249.3 billion while the external trade deficit with non-EU countries was CZK 169.8 billion, with the latter being due to the trade deficits with other countries (CZK 88.8 billion), the CIS (CZK 29.2 billion), other developed market economies (CZK 32.7 billion) and developing economies (CZK 23.8 billion). European transition economies and EFTA States curbed the overall trade deficit with non-EU countries by the surpluses of CZK 5.4 billion and CZK 2.1 billion respectively.

The trade balance and its year-on-year increases/decreases in the individual groups of countries reflected the situation of the external trade balance with the main partner countries. The overall external balance surplus with EU countries was largely influenced (CZK 196.8 billion) by the favourable trade balance with five countries (Germany, Slovakia, the United Kingdom, France and Austria), which was up by CZK 26.6 billion y/y. Of the overall trade balance deficit with non-EU countries, a deficit of CZK 145.0 billion, as opposed to CZK 173.0 billion in the first half of 2008, was generated with three countries (China, Russia and Japan).

Commodity structure of external trade in the first half of 2009, compared to the same period of 2008, showed a decline of exports and imports in the overwhelming majority of SITC sections. Compared to the first half of 2008, the changes in the commodity structure in the first half of 2009 were characterised in:

- machinery and transport equipment by a decline in exports and imports by more than a fifth. The share of ‘machinery and transport equipment’ decreased in both total exports and total imports. Exports and imports of ‘machinery and transport equipment’ fell by 21.0% y/y (CZK 149.2 billion) and by 23.5% y/y (CZK 121.1 billion) respectively. The absolute decline in exports and imports was the greatest of all SITC sections, and thus significantly influenced the overall decline in external trade. The trade surplus in ‘machinery and transport equipment’ reached CZK 165.3 billion as opposed to CZK 193.4 billion in the first half of 2008 (with EU countries, it was CZK 231.1 billion as opposed to CZK 256.7 billion). All groups of machinery showed favourable trade balances. The highest external trade surplus was obvious in ‘road vehicles’, followed by ‘general industrial machinery and equipment’, ‘office machines and automatic data-processing machines’, ‘telecommunications and sound-recording equipment’, ‘other transport equipment’ and ‘power-generating machinery and equipment’;

- manufactured goods classified chiefly by material by decreasing exports and particularly imports. The share of these products decreased in both total exports and total imports. The trade surplus in those products rose to CZK 16.7 billion from CZK 3.3 billion in the first half of 2008. The trade balance improvement was primarily due to the decline in the trade deficit in ‘non-ferrous metals’ by CZK 11.7 billion and in ‘iron and steel’ by CZK 8.0 billion. The largest trade surpluses were generated in the ‘manufactures of metals’, ‘non-metallic mineral manufactures’ and ‘rubber manufactures’;

- miscellaneous manufactured articles, commodities and transactions not classified elsewhere in the SITC by a decrease in exports and imports, a decrease in the external trade surplus by CZK 6.9 billion and the increased share of both total exports and total imports. A surplus was posted by the trade in ‘miscellaneous manufactured articles, n.e.s.’, ‘furniture and parts thereof’, ‘prefabricated buildings’ and ‘sanitary, plumbing, heating and lighting fixtures and fittings, n.e.s.’. The trade deficit decreased in ‘professional, scientific and controlling instruments and apparatus, n.e.s.’ and increased in ‘articles of apparel and clothing accessories’ and ‘footwear’;

- chemicals and related products by decreases in exports and imports and a moderate increase in their shares of both total exports and total imports. The trade deficit was the second highest (CZK 45.5 billion), though CZK 8.0 billion y/y lower. The high deficit continued to centre upon ‘medicinal and pharmaceutical products’, and rose by CZK 1.7 billion y/y. The trade deficit fell in ‘plastics in primary forms’ by CZK 4.2 billion, ‘plastics in non-primary forms’ by CZK 1.5 billion, ‘chemical materials and products, n.e.s.’ by CZK 1.6 billion and ‘dyeing, tanning and colouring materials’ by CZK 0.9 billion;

- crude materials, inedible, and mineral fuels by decreasing exports and especially imports. The trade deficit fell by CZK 32.4 billion, but continued to be the highest of all SITC sections (CZK 47.4 billion). The deficit primarily improved due to a lower trade deficit in ‘petroleum, petroleum products and related materials’ by CZK 24.0 billion. Imports of this commodity item fell by 41.8% y/y (petroleum imports fell by 4.3% in volume and by 44.1% in value). The balance of trade in ‘crude materials, inedible, and mineral fuels’ was affected by the increase in trade deficit in ‘gas, natural and manufactured’ by CZK 2,7 billion (natural gas imports fell by 22.5% in volume and by 1.7% in value) and by the decrease in the trade surplus in ‘coal, coke and briquettes’ by CZK 3.5 billion. A positive effect was the increase in the trade surplus in ‘electric current’ by CZK 4.1 billion, the deficit in ‘metalliferous ores and metal scrap’ turning into a surplus, and the persisting trade surplus in ‘cork and wood’;

- agricultural and food crude materials and products by decreasing exports and, as the only SITC section, by increasing imports. The trade deficit grew by CZK 3.6 billion y/y. The largest trade deficit was posted in ‘vegetables and fruit’ and in ‘meat and meat preparations’. The trade surplus in ‘cereals and cereal preparations’ rose by CZK 2.3 billion; the trade surplus in ‘tobacco and tobacco manufactures’ decreased by CZK 1.1 billion, as did the trade surplus in ‘dairy products and birds eggs’ by CZK 1.5 billion.

| Sections of SITC, rev. 4 | Sections of SITC, rev. 4 | ||

| 0+1+4 | Agricultural and food crude materials and products | 6 | Manufactured goods classified chiefly by material |

| 2+3 | Crude materials, inedible, and mineral fuels | 7 | Machinery and transport equipment |

| 5 | Chemicals and related products | 8+9 | Miscellaneous manufactured articles, commodities and transactions not classified elsewhere in the SITC |

o - o - o

On 17 July 2009, Eurostat released data on the external trade of EU countries for January-April 2009. All EU countries (except Ireland) saw double-digit decreases in their respective external trade turnovers compared to the same period of 2008. The Czech Republic’s exports fell somewhat more year-on-year than the exports of EU countries in total as well as the exports of new EU Member States; the Czech Republic’s imports decreased more year-on-year than EU imports in total and less than the imports of new EU Member States. In January-April 2009, EU27 (EU15) exports in EUR declined by 23.1% (22.9%) y/y on average while EU27 (EU15) imports in EUR fell by 23.2% (22.2%) y/y on average. The average year-on-year exports and imports of the 12 new Member States fell by 24.7% and 30.4% respectively. In January-April 2009, the share of the 12 new EU Member States in overall EU exports increased to 10.7% from 10.1% in January-April 2008 while their shares of overall EU imports for the same periods were 11.1% and 12.3% respectively. In January-April 2009, the EU27 trade balance posted a deficit of EUR 30.1 billion (the deficits of the EU15 and of the 12 new EU Member States were EUR 22.3 billion and EUR 7.8 billion respectively), which means a decrease by EUR 11.8 billion y/y. The Czech Republic (just as ten other EU countries) showed a trade balance surplus in January-April 2009. Of the new EU Member States, Slovakia also showed a trade balance surplus (although much lower, EUR 0.1 billion) for the said period and Slovenia’s trade balance was in equilibrium.

1 All data are at current prices. Data for 2008 are updated, referring to the 1 June 2009 closing date. Data for January-March 2009 are updated, referring to the 1 June 2009 closing date; data for April are preliminary, referring to the 1 June 2009 closing date, data for May are preliminary, referring to the 26 June 2009 closing date; and data for June are preliminary, referring to the 29 July 2009 closing date. The published data is processed in basic units and then rounded, which may give rise to discrepancies.

2 The external trade turnover (though much less significant) also fell in the first half of 2002, by 3.9% year-on-year (exports were down by 1.8% and imports down by 5.9%).

3 In the first half of 2008, the trade surplus was CZK 64.1 billion.

4 In January-June 2009, compared to January-June 2008, CZK weakened by 7.2% and 19.2% on average against EUR and USD respectively. In January-June 2008, compared to January-June 2007, CZK strengthened by 11.7% and 28.5% on average against EUR and USD respectively.

5 The Commonwealth of Independent States.

6 China, North Korea, Cuba, Laos, Mongolia and Vietnam.

7 Items of CZ-CPA (Classification of Products by Activity) 15 to 36.

8 Import and export price indices in the Czech Republic are published a month later than data on the external trade of the Czech Republic.